23 March 2020 | Technical

This outline sets out the main measures enacted and is not exhaustive. We would be very pleased to assist should you have any specific query.

GENERAL TERMS:

The Covid 19 period covers the period from 23 March 2020 to 1 June 2020. However, the period may be extended to any other date prescribed by way of regulations.

CORPORATE AND INSOLVENCY MEASURES

- Any licence expiring during the COVID-19 period or 30 days after the end of the COVID-19 period will be deemed valid until such time as is prescribed by the individual act governing that licence. Accordingly, no penalties, surcharges or additional fees will apply during the above period. We set out examples that may be of interest below:

- The deadline for renewal of licences will also be extended for:

- EIA licences;

- Tourist accommodation certificate;

- Tourist enterprise licence;

- Pleasure craft licence and other licences under the Tourism Authority Act;

- Licences under the Gambling Regulatory Authority Act.

- under Information and Communication Technologies Act

2) Practice directions to be issued

- The Registrar of Companies may issue Practice Directions and other guidelines or instructions that it will publish in the Gazette. This will apply to the Foundations Act, Limited Liability Partnerships Act.

- Whilst the purpose of the Practice Directions is not explicit, it can be inferred that they will assist with the administration of corporate matters during and in the aftermath of the COVID-19 period.

3) Annual Shareholder’ Meetings

- Annual meetings of shareholders will be held within 9 months of the balance sheet date of the company instead of 6 months unless otherwise prescribed by the Registrar of Companies.

- In addition, during the COVID-19 period (which may be extended by the Registrar of Companies), the statutory requirements of holding a shareholders’ meeting between 12 and 15 months of the previous one will not apply.

4) Filing of financial statements

- The time limit to prepare financial statements and register them has been extended from 6 months to 9 months from the end of Covid19 period and the time limit to register them has been extended from 28 days to 3 months after the Covid19 period ends.

- It appears that the time limit for companies filing their tax returns is still 6 months after the year end of the company. This lack of synchronicity may lead to delays in filing tax returns in cases where the final financial statements are not ready by the tax deadline.

5) Financial Services Act

- The Board of the Financial Services Commission may be held either through a meeting of the quorum or by virtual means (audio or visual communication) so long as participating members form a quorum.

6) Insolvency measures

- The amount of unpaid debt limit for the Courts and creditors to petition for bankruptcy has been increased from Rs 50,000 to Rs 100,000.

- Any resolution to wind up a company during the Covid-19 period and within 3 months of the end of the COVID-19 period is not valid, except for companies holding a Global Business Licence. The exemption does not include Authorised Companies.

- The appointment of receiver or manager during the Covid-19 period is not valid.

- Creditors meetings will not be held during the COVID-19 period and 3 months thereafter for all companies.

- The statutory demand debt minimum has increased from MUR 100,000 to MUR 250,000. The period of compliance from service is extended from 1 month to 2 months and the limitation period for the application to set aside a statutory demand is now 28 days, up from 14 days.

- The first creditors’ meeting for companies under administration should take place within 30 days if the end of the COVID-19 period.

- The duty of directors during insolvency will not apply during the COVID-19 period.

TAX MEASURES

Companies and individuals who contributed to the Covid-19 Solidarity Fund will be able to deduct the amount donated to arrive at their net income in the income year of contribution.

Any unrelieved amount may be carried forward for a maximum of 2 years following the income year in which the contribution was made.

The definition of companies includes trusts, sociétés and foundations so that they will also be entitled to a deduction.

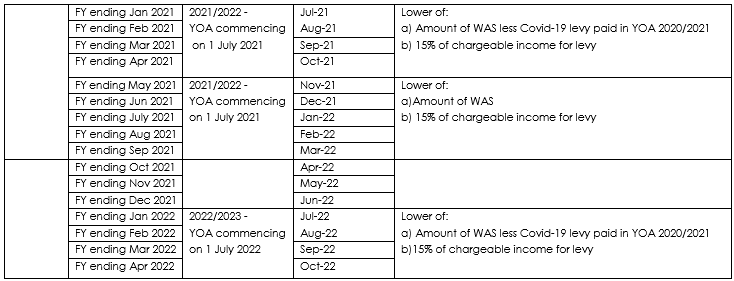

2) Wage Assistance Scheme

Under the scheme, an employer can apply for a repayable grant to pay part of the wages of qualifying employees during the lockdown period as set out below. Employers include charitable institutions. The term employees include Mauritian employees and expatriates working in Mauritius. It applies to both full time and part time employees.

*50% of this amount if the business activities of the employer are carried out in Rodrigues or Agaléga.

An employee will receive the national minimum wage of Rs 9,000 if they:

- are Mauritian citizen;

- are employed in an export manufacturing enterprise;

- are employed on a full-time basis; and

- their salary does not exceed the national minimum wage.

The grant made to any employer is repayable in the form of the COVID-19 levy.

Applications should be made within 3 months of the wage month it relates to or within 2 months of the end of the COVID-19 period.

An employer will be disqualified from using the scheme if:

- They terminate the employment of a WAS employee;

- They do not pay the wage to the employee; or

- They reduce the salary of the WAS employee.

The employer will be required to reimburse the allowance claimed in the last 2 cases above.

3) Self-employed Assistance Scheme

The scheme applies to tradespersons specifically such as masonry, cabinet makers, plumbers, hairdressers and artists who have been operating their business at least 3 months prior to the COVID-19 period and whose monthly income plus that of his spouse, amounts to Rs 50,000 or less.

The scheme does not apply to individuals:

- that are part-time employees

- deriving passive income (landlords, investors generating interest or dividend income)

- receiving social benefits including basic retirement pension;

- pursuing higher studies on a full-time basis;

- Dependent spouses;

- Registered fishermen.

Applications should be made within 3 months of the wage month it relates to or within 2 months of the end of the COVID-19 period.

The MRA is entitled to request verification documents pertaining to the self-employed’s application within a year of making payment of the allowance.

The MRA has the right to recover the amount advanced if it deems that the individual’s claim is incorrect or in excess.

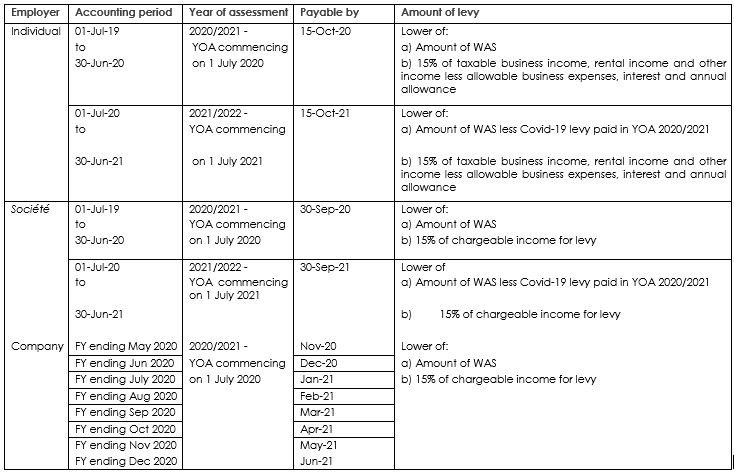

4) Covid-19 Levy

Employers claiming the Wage Assistance Scheme (“WAS”) will be subject to the COVID-19 levy

The levy is calculated as the lower of:

- the amount of the Wage Assistance received under the scheme; and

- 15% of the chargeable income of the company as calculated for levy purposes. The chargeable income for levy purposes excludes unrelieved tax losses brought forward from previous years of assessment.

The levy will be payable at the time the annual tax return is filed according to the year of assessment as set out in Appendix 1.

The levy is payable at the time the annual tax return is filed.

Certain categories of employers may be excluded from the levy by way of regulations.

Failure to pay the levy will lead to penalty of 10% and interest of 1% per month or part of the month during which the levy remains unpaid.

As the legislation is currently drafted, there are no provisions for further repayments to the MRA through the COVID-19 levy should the employer not have reimbursed the total amount of wage assistance received by YOA 2021/22 for individuals and sociétés and YOA 2022/23 for companies.

5) Proceedings before the Assessment Review Committee (“ARC”)

The statutory delay in relation to proceedings before the ARC that falls or expires during the COVID-19 period has extended to start at the end of the COVID-19 period.

If the statutory delay falls within 21 days of the end of the COVID-19 period, the statutory delay will start after the 21-day period.

6) Extension of statutory time limits for assessments and claim

If the time limit to issue an assessment, determination, notice, take a decision or make a claim under any Revenue Law falls within the COVID-19 period or 30 days after the end of the COVID-19 period, the time limits will be extended by 2 months after the end of the COVID-19 period and 2 months after the end of the 30 days respectively.

7) Extension of payment deadlines

If a payment under revenue law (income tax, PAYE, VAT, excise duty) is due during the COVID-19 period, the taxpayer will not incur penalties or interest if payment is made by 25 June 2020.

If payment is due between the end of the COVID-19 period and 30 June 2020, the taxpayer should make the payment by 26 June 2020 i.e. there is no extension for taxpayers who have tax payable due for June 2020 (for example companies with a 31 December 2019 year-end).

8) Deadline extension for the Expeditious Dispute Resolution Tax Scheme Panel

An applicant has until 31 August 2020 to make an application to the panel. The previous deadline was 30 June 2020.

9) Portable Retirement Gratuity Fund

The application of the PRGF has been reported until further notice. However, regulations will be issued to set out the amount the employer will pay to the employee if the employee retires, resigns, is terminated or dies on 1 January 2020 or after

10) VAT measures

The following products have been included as zero-rated for Valued Added Tax purposes: Protective masks against dust, odours and the like, other breathing appliances and gas masks, hand sanitisers.

11) Customs duty on cleared goods

- The duty, excise duty, taxes and any fees payable on cleared goods is extended from 7 days to 16 days.

- If goods entered during the period between 2 November 2019 and 31 December 2020, they can be stored in bonded warehouses from the date of entry for 36 months, up from 24 months.

12) Disinfectants at 0% duty

- There will be 0% duty on disinfectants including hand sanitisers (HS Code 3808.94.00) as well as ‘other’ related products.

13) Registration duty

The surcharge and penalty payable when a deed is presented or registered outside the time limits specified in the Sixth Schedule of the Act will not apply if the time limit fell within the COVID-19 period or any period as may be prescribed.

REAL ESTATE MEASURES

- The non-payment of rent for commercial and residential leases for the months of March to August 2020 does not constitute a breach of a tenancy agreement provided the rent is paid in full by 31 December 2021.

2) Land and Duties Taxes

- Payment of duty or tax

If the 28-day period to pay duty or tax falls within the COVID-19 period or 21 days after the end of the COVID-19 period, the deadline will be extended to 28 days and 49 days after the end of the COVID-19 period respectively.

- Notice of assessment

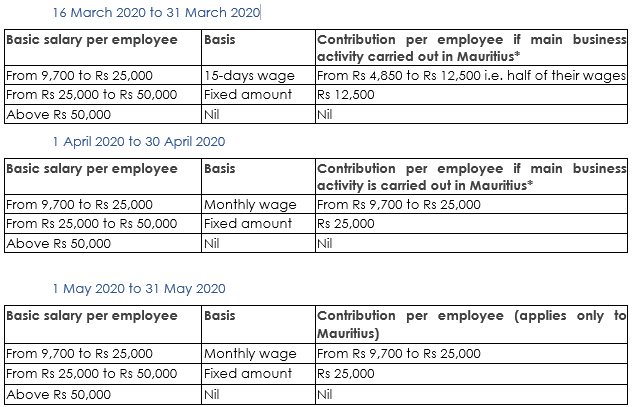

If a notice of assessment falls within the COVID-19 period or within 1 month of the end of the COVID-19 period, the Registrar General will have an additional 3 months after the end of the COVID-19 period to send the notice.

EMPLOYMENT MEASURES

- A worker may be required to work from home provided a notice of at least 48 hours is given by the employer.

- An employer may ask a worker to work on flexitime. A worker may also request to work on flexitime regardless of the reasons.

2) Annual leave deduction

- Employers can deduct up to 15 days of annual leave from the total leave aggregated between 1 January 2020 to the end of the COVID-19 period during the 18 months following the expiry of the Covid-19 i.e. between June 2020 and November 2021. If a worker was working in the period between 23 March and 1 June, no annual leave deduction is applicable.

3) Reduction of workforce

- Employers operating in specified sectors that require a minimum service (e.g. air traffic control, civil aviation, hotel services, transport of passengers and goods) may be able to use an express process if they need to reduce their workforce by applying to the Remuneration Board without need to notify the employee. If the Board finds that the employer’s grounds are justified, the payment of severance allowance of 3 months’ remuneration per year of service may be restricted to 30 days’ wages as indemnity in lieu of notice. The Board may also allow that in lieu of termination of the employment and with the consent of the worker, the worker shall proceed on leave without pay for a specified period and the resumption of employment may be on new terms and conditions.

4) Other employment measures

- No allowance will be paid for work performed on night shift from 16 May 2020 until further notice.

- Workers in the construction and manufacturing industries governed by the Factory Employees (Remuneration) Regulations 2019 will be entitled to compensation during the COVID-19 period under prescribed rates.

OTHER GENERAL MEASURES

Permits issued under Immigration Act that expired during the Covid-19 period or 21 days after the Covid-19 period is extended for a further period of 30 days after the Covid -19 period lapses.

2) Continuing Professional Development (“CPD”)

Individuals required to undertake CPD courses for continued registration to carry out their professions will be exempt from the requirement during the current year.

Appendix 1